Property intelligence firm, Charter Keck Cramer in association with the Urban Development Institute of Australia recently published a report titled ‘Melbourne Apartment Market Snapshot’ dated August 2015.

The report provides a number of key findings with regard to the growth, supply and evolving trends of apartments within Australia’s second largest City, Melbourne.

Here is a summary of key findings as prescribed in the paper:

“There is no doubt that the structure of Melbourne’s housing market has fundamentally shifted since the mid-1990s. This change is due to the advent of contemporary apartments becoming a legitimate, and increasingly since 2010, preferred form of housing for a broadening range of households”.

Maturity:

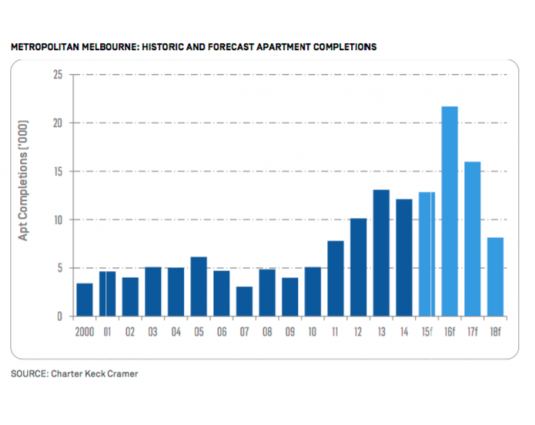

Apartment stock in Melbourne has experienced rapid expansion, from 63,000 apartments in 2010 to 112,000 in 2015.

This trend is set to continue increasing with an estimated 15,000 new apartments completed per annum, with projections for the City to have 160,000 by 2018.

Supply Distribution:

Whilst general perceptions portray Melbourne’s blossoming CBD as the key proportion of new apartment builds, research highlights that only 38% of completed apartments are actually contained within the Central City.

A further 31% are located within the City Fringe, generally understood as 2-5km radius of the CBD, in addition to 19% in the Inner Precincts, considered 5-10km from the CBD.

Increasingly, it is presumed that these figures will experience an even greater shift, with land sites in the CBD becoming increasingly unattainable, and thus developers focusing their sites in areas of strong population growth, efficient transport networks, and more complementary zoning and land availability.

Utilising a sample of recently released projects across the Melbourne and Fringe Melbourne markets, a general apartment median price can be extracted.

- One bedroom $400,000

- Two bedroom $570,000

National Context:

In the period 2010 - 2014, Melbourne’s booming apartment market accounted for no less than 47% of Australia’s Core Capital City apartment supply.

The report suggests that for the next period, 2015 - 2019, Melbourne will continue to account for 44% of this national supply.

Further information can be viewed by visiting:

With thanks to UDIA & Charter Keck Cramer.