After a few years of abnormal investment activity, the market is levelling back out, and consistent, gradual growth is back on the cards.

Offshore investment is a constant and divisive topic in the world of commercial property, and as such, articles like CBRE’s In and Out Australia report occupy the interest of the industry at large. The most recent release in the series deconstructs exactly where inbound capital has been originating from for the first half of 2022, and some of the identifiable trends might prove surprising.

Offshore investors are re-embracing office

2021 was an unusual year in the sense that the Industrial and Logistics (I&L) sector was the most active out of the four categories being tracked for offshore investment, which can be credited to “the significant amount of portfolio deals in early 2021”, according to CBRE’s report. Besides 2021, the office has remained the consistent stalwart, serving as the favoured asset class for inbound capital year after year.

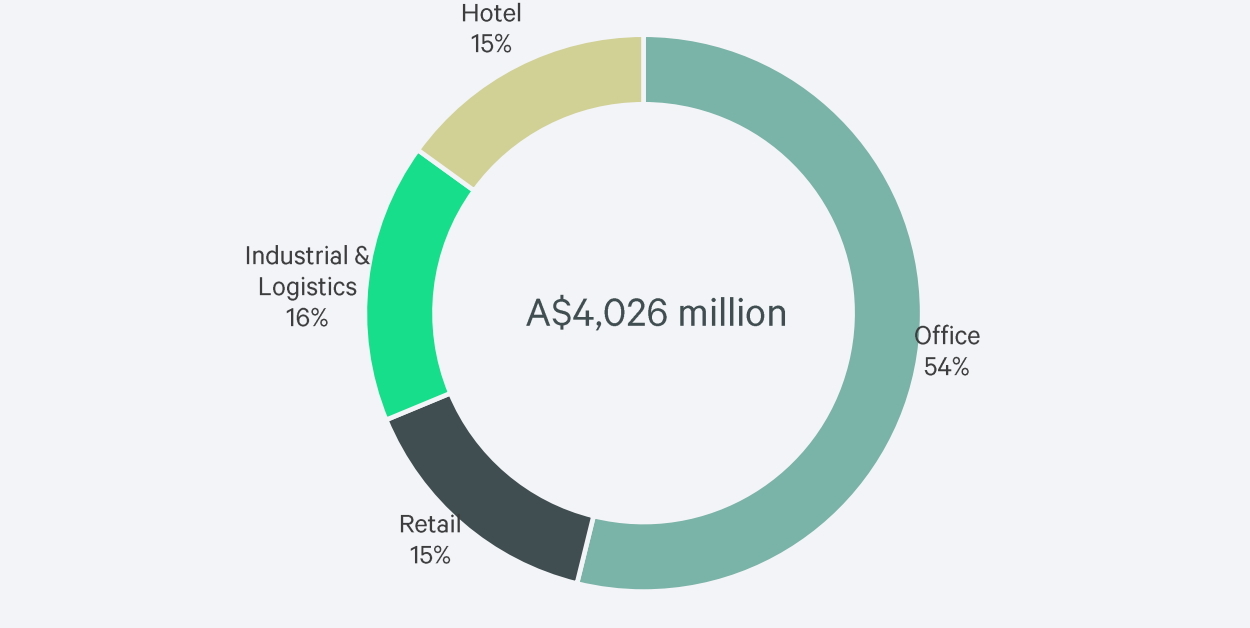

For the first half of 2022, 54% of inbound investment was concentrated on this sector. Alternatively, 15% went into hotels, 16% into I&L, and 15% into retail. Office was the overwhelming favourite amongst internationally-based investors.

Sector breakdown of offshore investment in H1 2022 - CBRE Research

We reached out to CBRE’s Head of Office and Capital Markets Research, Tom Broderick, for further comment, and he attributes much of the dominance of the office to scale.

“I think scale is one of the major reasons,” Broderick states. “Large CBD assets are generally worth greater than $200 million, which is what offshore groups are generally looking for. Deploying the same $200 million into individual I&L assets would require probably 4-5 different transactions.”

This explains why the I&L sector experienced a massive uptick in 2021; the portfolio opportunities available to international groups were much bigger than the standard I&L fare that Australia typically offers. But with less of these major portfolios being offered throughout the first half of 2022, the office has returned to prominence.

A $641 million boost from Hong Kong

In the first half of 2021, investment from Hong Kong totalled approximately $700 million. That figure nearly doubled in H1 2022, as Hong Kong-based volume reached $1.3 billion. The change year-on-year represents an increase of $641 million.

Offshore capital sources in H1 2022 - CBRE Research

“Since 2020, Australia has been the 2nd most popular destination globally, behind only Mainland China, for Hong Kong outbound capital investing into commercial real estate,” according to the report. Mr. Broderick explained why this is.

“Some Hong Kong groups seem to be wanting to diversify their portfolios across the APAC region and the world. These groups have a large weighting to their local market, so it makes sense to diversify. Australia is a key destination for this capital.”

Hong Kong is now investing more into Australia than any other country, and if Broderick’s analysis is accurate, these numbers don’t seem likely to subside soon.

Singapore’s massive drop

Despite standing out as the second largest source market for investment into Australia, volumes from Singapore were down considerably when compared to 2021.

The change year-on-year represented a decrease of $3.25 billion flowing into Australia from Singapore alone. Singapore and Canada are the only two capital sources mentioned in the report that had a negative year-on-year shift of $1 billion or more.

Whilst these numbers might initially seem alarming, Broderick explains that this is simply a result of “a very high base.”

“There were some significant purchases by Singaporean investors in H1 2021, and less so in H1 2022. I don’t think this is a trend, with Singapore continuing to be a key source of capital for the Australian commercial property market.”

With major groups like GIC having shown an overwhelming affinity for the Australian market, the year-on-year figure should play second fiddle to the overall volume, as whilst the change throughout the first half of 2022 has been large, it’s evident that Singapore remains as engaged as ever in Australia.

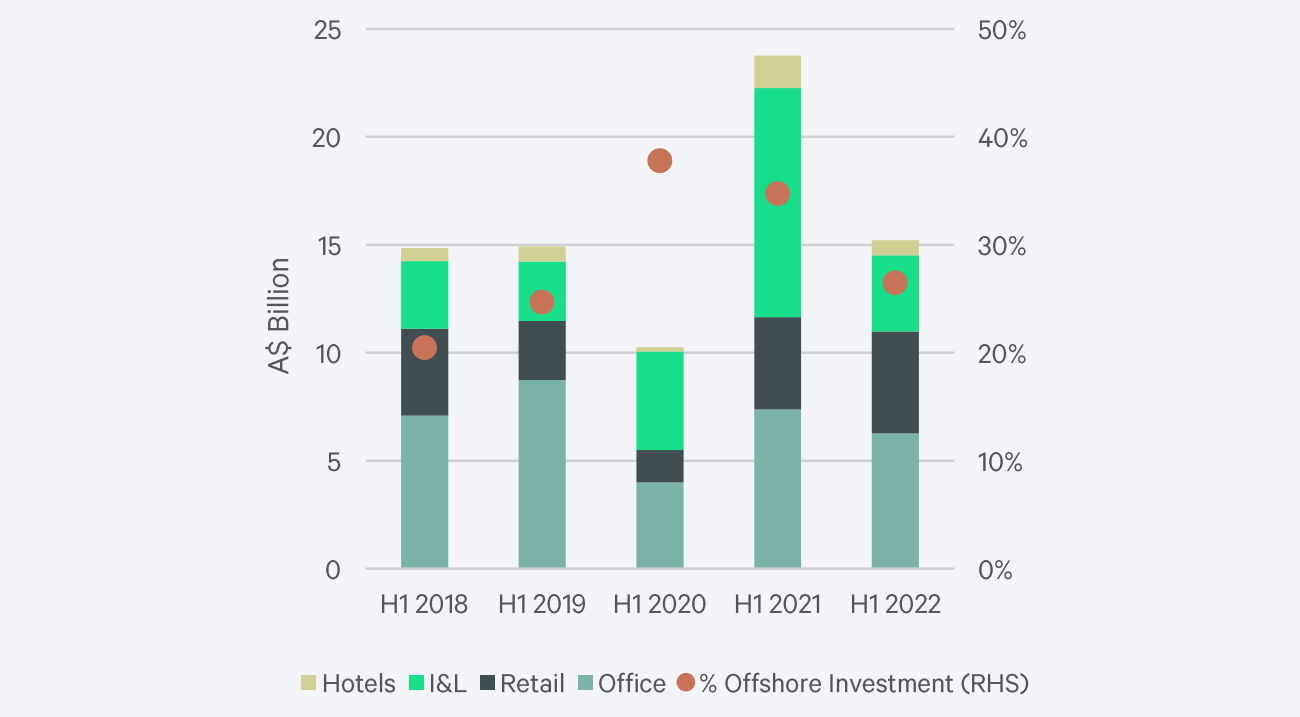

Offshore investment volumes are aligning with pre-pandemic figures

In both 2020 and 2021, overseas investors jumped on the opportunity to purchase property in Australia. In H1 2020, offshore investment accounted for just shy of 40% of total volumes; in H1 2021, that figure dropped marginally, down to 35%. Now, the percentages have normalised.

H1 volumes by sector and % offshore investment - CBRE Research

For the first half of 2022, inbound capital represented 26% of the total volume invested in the commercial property space, which is just a few percentage points higher than the figures reported in H1 2018 and H1 2019.

As such, after a few years of abnormal investment activity, the market is levelling back out, and consistent, gradual growth is back on the cards. $4.026 billion in offshore investment was recorded during H1 2022, and with continued interest from sources like Singapore, Hong Kong, and the USA, that figure seems poised to continue to grow over the next few years.